ABW MEDIA & EDUCATION HUB

WELCOME TO THE DEDICATED RESOURCES PAGE FOR ALL A BETTER WAY MORTGAGE GROUP MEDIA AND EDUCATIONAL CONTENT

HERE YOU WILL FIND:

- ABW Tuesday Memo: Posted weekly, providing valuable insights, updates, and trends in the mortgage industry.

- The Mortgage Broker Podcast: Access all episodes, featuring expert discussions, tips, and strategies to help you succeed.

This hub is designed to keep you informed, inspired, and equipped with the tools you need to grow and excel in your business. Explore, learn, and stay ahead with ABW.

Episode 59 — Broker Armour #1: FINTRAC One Year Later (Are You Protected?) SERIES LAUNCH: Broker Armour HOSTS: Dean Lawton & Justin Noda (Chief Compliance & Operations Officer, ABW) What This Episode Covers Episode 59 kicks off Broker Armor, a brand-new series built specifically to help Canadian mortgage brokers stay protected, prepared, and compliant in a rapidly tightening regulatory environment. Dean sets the stage for what this series will become: a monthly (or more) “compliance home base” covering FINTRAC, provincial regulators, and upcoming changes—especially in BC with the MSA/BCFSA evolution. This first episode is deliberately “foundational.” Dean and Justin focus on one of the biggest points of confusion in the industry: FINTRAC’s requirements are primarily aimed at the brokerage (the reporting entity), not the individual agent—yet agents still carry meaningful responsibility inside each file. The conversation walks through a practical checklist that clearly separates brokerage responsibilities vs. broker responsibilities, with real-world examples of what gets missed, what triggers risk, and what could cause major issues during an audit. A downloadable checklist is mentioned in the show notes as a take-home tool that brokers and owners can use to self-audit their readiness. The Big “Aha”: Brokerage vs. Agent Responsibilities Justin makes it crystal clear early: FINTRAC refers to “reporting entities,” and that means the brokerage . This matters because the brokerage must register, access the FINTRAC web reporting system, build programs, train agents, keep records, and file reports. Agents should not be filing reports directly. Instead, agents are expected to follow the brokerage’s procedures, complete the KYC steps correctly, and escalate anything suspicious. This single distinction can expose a huge gap in many brokerages. If a broker doesn’t know who their compliance/AML lead is, doesn’t know where the policies are, or hasn’t been trained beyond the initial rollout in October 2024, that’s not just an education issue—it’s a risk issue. Broker ArmoUr Checklist — What Needs to Exist (and Who Owns It) 1. Appointed Compliance / AML Officer (Brokerage Responsibility) A major theme: this role can’t be an afterthought anymore. Justin explains that many firms historically treated compliance as part-time admin work. In today’s environment, that approach is dangerous. The compliance lead needs to be someone who is genuinely engaged, capable, and supported—because the workload is real, audits are coming, and the expectations are rising. Broker responsibility: know who this person is, respect the process, and actually use them as a resource. A simple self-check mentioned in spirit: Do you know your compliance officer’s name today? 2. Written Policies & Procedures Manual (PPM) — Brokerage Builds It / Brokers Follow It The PPM is effectively the brokerage’s FINTRAC “playbook.” It lays out how the brokerage interprets the rules and how brokers are expected to operate inside the program (ID methods, enhanced due diligence, documentation, escalation, etc.). Justin makes a key point: FINTRAC rules are clear, but the “how” can vary—so each brokerage must define their approach and then operate consistently. Broker responsibility: read it, acknowledge it, follow it. (And if your brokerage can’t easily provide it, that’s an immediate red flag.) 3. Risk-Based Assessment (RBA) — Brokerage Defines Risk Appetite / Brokers Need to Understand It Justin distinguishes two commonly confused items: RBA (Risk-Based Assessment): brokerage-level document that defines the firm’s risk appetite and approach Client Risk Assessment: file-level decision brokers make (high/medium/low risk) The RBA informs how the brokerage wants risk measured and what steps are required when risk increases. Justin explains how ABW built tools (like a scorecard approach) to drive consistent risk ratings and reduce “gut-feel only” decisions—because inconsistency creates exposure in audits. Broker responsibility: understand the risk factors and collect the info needed to rate a file properly. 4. Ongoing Training Program (Brokerage Must Run It / Brokers Must Complete It) This episode strongly reinforces: training isn’t a one-time rollout. Brokerages need an annual training program, documented and trackable, so they can prove education happened if issues arise later. Justin notes many firms haven’t built this properly yet because “the year felt far away”—but FINTRAC’s expectations are now moving into the “you should know this by now” stage. Broker responsibility: complete the training and apply it in real files. The subtext is important: ignorance won’t be a defensible position going forward. 5. Two-Year Effectiveness Review (Brokerage Responsibility — and It’s Coming Fast) This one is a major “heads up.” FINTRAC requires a formal effectiveness review every two years, where an appropriately qualified reviewer evaluates whether the brokerage program actually works. It can’t be done by the same person who built the program, and it’s often not cheap—Justin notes it can run well into five figures depending on scope and size. Broker responsibility: none directly—other than cooperating if asked and adapting to changes that follow the review. 6. Client ID + Beneficial Ownership (Shared Responsibility) This is where brokers feel FINTRAC most day-to-day. Client ID must follow an approved method (and must be valid/current). Justin shares examples of how things go sideways when brokers treat ID casually. Beneficial ownership becomes critical in business-for-self files or corporate entities, especially where someone owns 25%+ but isn’t on the mortgage. That’s not an automatic “no”—it’s a documentation and transparency requirement. Brokerage responsibility: define acceptable methods and provide tools/process Broker responsibility: execute correctly, document properly, and do it early (not at the end) 7. PEP / HIO Screening + Sanctions (Shared Responsibility) This is another major pillar: screening for Politically Exposed Persons (PEPs) and Heads of International Organizations (HIOs), plus sanctions checks. Justin explains that the brokerage must provide the mechanism (forms, platform tools, or paid screening options), but brokers must actually run it and escalate when results require extra due diligence. A key nuance highlighted: foreign vs. domestic PEPs are treated differently, and when a potential match appears, brokers may need to do deeper confirmation (e.g., verifying it’s a different person with the same name). Justin shares that the work can get unexpectedly serious—examples included links to sanctioned geographies, adverse media, and crypto-related laundering attempts. The point is clear: these aren’t theoretical risks anymore. 8. Ongoing Monitoring + Suspicious Activity (Mostly Brokerage, But Brokers Must Be Alert) Justin explains ongoing monitoring is largely brokerage-driven and is typically tied to the risk rating: high-risk clients may require more frequent re-checks. Brokers don’t run monitoring programs, but brokers absolutely impact them by assigning accurate risk levels at the start and flagging anything unusual. For suspicious activity: brokers are the “front line.” If something feels off, brokers should escalate internally—never ignore it, never try to quietly push a file through. 9. Record Keeping (5+ Years) — Shared Responsibility This is straightforward but critical: brokerages must securely store required documents for 5+ years, and brokers must ensure the documentation is complete and uploaded properly. A future audit will compare what’s in your PPM/RBA against what’s in your actual files. 10. Reporting to FINTRAC (Brokerage Only) Justin reinforces a common misconception: brokers do not file FINTRAC reports directly. Broker responsibility is to raise concerns internally using the brokerage’s process (internal STR form, escalation workflow, etc.). The brokerage then decides whether to file official reports through the FINTRAC reporting system. 11. FINTRAC Examinations / Audits (They’re Already Starting) This is the tone-setter near the end: audits have begun, and while the early phase may not be “hammer down,” FINTRAC is making expectations known. Justin also notes proposed legislative changes that could massively increase penalties—making today’s discipline the difference between a manageable process and a catastrophic one later. Dean adds a key industry-level point: if someone gets made an example of, it’s not just bad for them—it’s bad for the entire channel. 11. FINTRAC Examinations / Audits (They’re Already Starting) Justin notes most brokers now understand the “standard pillars” (ID, PEP, sanctions, basic risk rating), but where gaps show up is in the deeper risk logic—things like: Beneficial ownership and corporate control Third-party involvement (who is really directing the transaction) High-risk industries or unusual sources of funds Risk patterns that don’t show up in the obvious checklist items His framing is useful: these risks always existed—brokers are just being forced to see them clearly now. Action Steps for Brokers This Week If you want this episode to actually protect you (not just educate you), here’s the practical follow-through that aligns with what Dean and Justin are pushing: Download the checklist and walk through it with your brokerage in mind Confirm you know your compliance/AML lead and how to escalate concerns Ask where your PPM + RBA live and whether you’ve acknowledged them Make sure your ID method is brokerage-approved (and documented correctly) Stop treating risk assessment like “gut feel” —collect the facts that support the rating Escalate anything that feels off early (before it becomes a “cleanup after the fact” situation) Justin also openly invites brokers and broker owners to reach out confidentially if they’re unsure whether their current setup is truly compliant. Why You Should Listen This episode is a reality check—and a protection plan. If you’re treating FINTRAC as a “box-checking exercise,” you’re exposed. Justin breaks down what FINTRAC actually expects, what your brokerage must have in place, what you personally must execute inside the file, and why audits (and penalties) are only getting stricter from here. If you want to keep your license safe , avoid becoming the brokerage that gets made an example of, and understand compliance in a way that’s practical—not theoretical—Episode 59 is required listening. For weekly market updates, sign up for the ABW Tuesday Mortgage Memo . If you’re a broker considering a network change or looking to grow, reach out to us to explore how we can support your success.

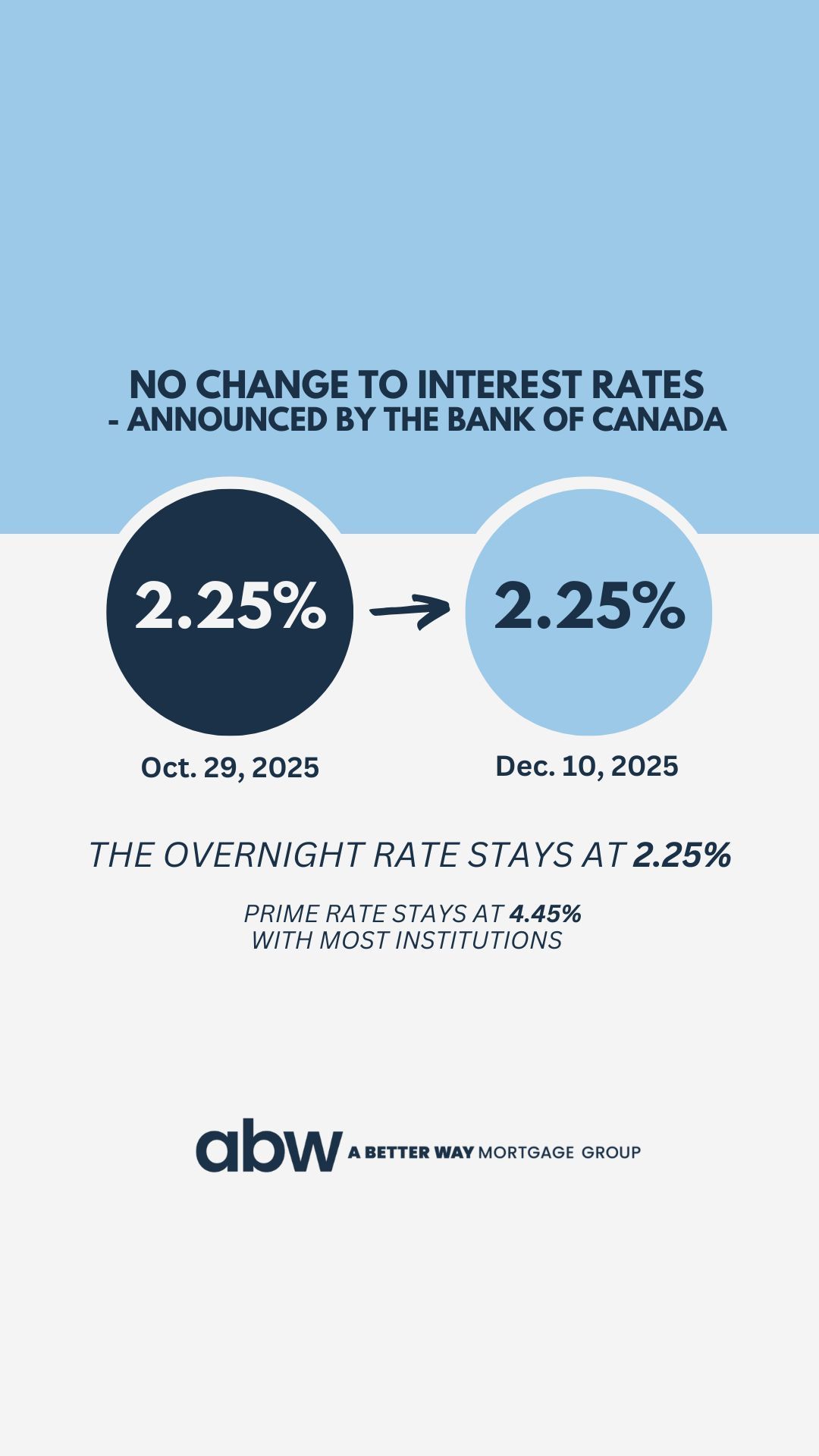

01/28/2026: BoC Holds at 2.25%: A Measured Pause as Policy Nears Its Destination

01/27/2026 Tuesday Mortgage Memo: Your Weekly Market Highlights

01/20/2026 Tuesday Mortgage Memo: Your Weekly Market Highlights

EPISODE 58: A Year in Review - National Leadership Team A Better Way Mortgage Group By: Dean, Jason & Deryk A Different Energy Entering 2026 2025 was a milestone year for A Better Way Mortgage Group—and this “Year in Review” episode pulls back the curtain on what actually drove the momentum. Dean, Jason, and Deryk reflect on a year that felt noticeably different than the previous cycle: more optimism, stronger broker engagement, better energy at events, and a renewed sense that the industry has found its rhythm again. They’re candid that this episode includes some celebration of the team’s wins—but the real intent is to share lessons, strategy, and what’s coming next for brokers who want to keep building in a changing market. Where the Market Shifted — And Where Opportunity Showed Up A big theme throughout the conversation is how brokers adapted to the realities of today’s lending environment. The team highlights a major shift toward alternative lending, private solutions, reverse mortgages, and a more strategic focus on where opportunity exists—especially in segments where brokers aren’t constantly competing with non-channel banks. They also unpack the “renewal wave” with a realistic lens: you’re not going to win every renewal, but the sheer volume of maturities means even a modest capture rate can materially change a broker’s year. The takeaway is simple: deals are still there, but brokers who win are the ones who stay educated, broaden their skill set, and lean into new lanes of business. The Numbers Behind the Record Year The stats tell the story of a brokerage that scaled—without losing structure. A Better Way funded $4.1B in 2025, up $1.3B year-over-year, and served 1,900+ additional families compared to the year prior. They also celebrate a protection milestone that matters: 300 more families secured mortgage protection insurance (MPP), reinforcing the brokerage’s focus on not just closing mortgages, but protecting clients long term. Growth came from both directions—existing agents expanding their books through training and tools, and new high-performing talent joining from other brokerages and bank channels. Scaling Without Chaos: Compliance, Ops, and Support Roles To support that level of production, the episode dives into the infrastructure upgrades made behind the scenes—particularly in compliance, onboarding, operations, and AML/FINTRAC readiness. The team outlines key hires and internal role improvements that helped strengthen the brokerage’s ability to scale responsibly, protect agents, and reduce friction. They also emphasize that training remains the backbone of the culture: 95 lender presentations, 22 business sessions, weekly internal updates, and the continued distribution of the ABW Tuesday Mortgage Memo—a public-facing market recap many brokers now repurpose into their own content and referral-partner communication. Community, Events, and Why Culture Drives Performance To close, the team previews a bigger year ahead—more podcast expansion (including Justin Noda’s upcoming “Broker Armor” series), more content formats (studio and virtual), more training opened to the broader industry, and deeper system improvements through DLCG tools and dedicated support. It’s equal parts reflection and roadmap—an inside look at what worked in 2025, why it worked, and how brokers can carry that momentum into 2026. Looking Ahead: More Content, More Training, More Tools On the tactical side, Alfredo breaks down what he uses daily: Velocity, Gold Rush CRM, Lender Spotlight, DocuSign, and Penalty Mentor for quick penalty estimates and client visuals. He also stresses the value of lender relationships—BDMs, underwriters, and mortgage teams aren’t barriers; they’re partners. His learning stack includes Mortgage Logic News, regulatory updates (including FSRA/FISRA), and using AI to summarize industry updates into client- and referral-partner-friendly talking points. Why You Should Listen If you’re a broker looking for a real-world playbook on how top teams are growing in a “tough” market, this episode is packed with practical insight. It’s not just numbers—it’s the strategy behind alternative growth, renewal opportunity, training discipline, compliance readiness, and building a culture that keeps brokers engaged, learning, and winning year after year. For weekly market updates, sign up for the ABW Tuesday Mortgage Memo . If you’re a broker considering a network change or looking to grow, reach out to us to explore how we can support your success.

01/13/2026 Tuesday Mortgage Memo: Your Weekly Market Highlights

EPISODE 57: Behind the Broker with Alfredo Torres Guest: Alfredo Torres Hosts: Dean Lawton & Jason Marshall From Service-First Roots to Mortgage Brokering Alfredo’s story starts long before mortgages—rooted in acts of service and a natural desire to help. From sweeping hair as a kid, to years at McDonald’s (including “McDonald’s University”), Alfredo learned early how systems, consistency, and customer experience shape success. That same mindset carried into a nine-year career at TD, where he built a strong foundation across lending, investments, and client communication. The Pivot: Leaving the Bank and Finding the Broker Path When bank “optimization” created uncertainty, Alfredo made a proactive decision: get ahead of the change and take ownership of his next chapter. What followed was an unexpected—and very organic—transition into brokering. A few mortgage brokers began reaching out, lunches turned into real conversations, and soon Alfredo was mapping out his exit strategy into a brokerage environment where he could keep growing while serving clients in a bigger way.. Why Alfredo Thrives at A Better Way A major theme in the episode is culture. Alfredo shares how refreshing it’s been to step into an environment built on support, trust, and growth without judgment. He highlights the advantage ABW brokers have with training and structure—especially the Perfect Loan Process—and points out a truth many overlook: the tools and resources are already available; the difference is the discipline to use them. The Top 50 leaderboard comes up as a powerful motivator too—not as pressure, but as a catalyst for accountability, community, and shared momentum. Communication as the Real Competitive Advantage One of the strongest segments dives into Alfredo’s approach to client relationships. His focus is on building rapport not just consciously, but unconsciously—by speaking in the “model of the world” clients naturally communicate in. He shares how understanding communication styles can instantly lower stress, build trust, and create a smoother experience—especially in chaotic or high-pressure files. With AI becoming more present in the industry, Alfredo believes emotional intelligence and human connection will be even more valuable going forward. Wins That Create Clients for Life Alfredo shares memorable success stories that underline the power of brokering. From helping clients buy homes back in the day with 100% financing options, to guiding people through credit rebuild journeys and returning them to A-lending, he emphasizes that a broker’s role isn’t just closing a deal—it’s building a plan. When clients feel supported through a multi-year path, loyalty becomes automatic, and referrals follow naturally. Tools, Tips, and Staying Sharp On the tactical side, Alfredo breaks down what he uses daily: Velocity, Gold Rush CRM, Lender Spotlight, DocuSign, and Penalty Mentor for quick penalty estimates and client visuals. He also stresses the value of lender relationships—BDMs, underwriters, and mortgage teams aren’t barriers; they’re partners. His learning stack includes Mortgage Logic News, regulatory updates (including FSRA/FISRA), and using AI to summarize industry updates into client- and referral-partner-friendly talking points. Why You Should Listen This episode is a reminder that brokering is still a relationship business—and the brokers who win long-term are the ones who combine structure, communication, and service. If you want practical insight on how to build client trust faster, create raving fans, use systems like a pro, and stay motivated through the grind while keeping your life in balance, Alfredo’s playbook is worth hearing. For weekly market updates, sign up for the ABW Tuesday Mortgage Memo . If you’re a broker considering a network change or looking to grow, reach out to us to explore how we can support your success.

12/16/2025 Tuesday Mortgage Memo: Your Weekly Market Highlights

EPISODE 56: Behind the Lender with Alex Dey, ScotiabanK Guest: Alex Dey, VP Portfolio Optimization, Scotiabank Hosts: Dean Lawton & Jason Marshall In this Behind the Lender episode, Alex Dey pulls back the curtain on how Scotiabank thinks about mortgages, capital, and the broker channel. With 22 years at the bank and more than a decade focused on mortgages, Alex oversees portfolio optimization, which means keeping the mortgage book growing, profitable, within risk appetite, and capital efficient. He explains why mortgages are considered an “anchor product” for the bank and why brokers are so central to that strategy. With roughly half of Canadians now choosing brokers, Scotiabank is committed to being present in every channel clients want to use, including branch, mobile specialists, digital, and the broker channel through the SMA model. Pricing, Liquidity Premiums, and a Wild Year for Rates One of the most educational parts of the episode is Alex’s breakdown of how a big bank actually prices mortgages. He explains that Scotiabank’s cost of funds has two main components: A base rate that tracks the bond market and can be hedged. A liquidity premium that reflects the extra risk the market assigns to bank funding and cannot be hedged. In the past year, total cost of funds moved roughly ten times more than the Bank of Canada’s overnight rate changes, with sharp spikes driven by politics, trade headlines, and market sentiment. Sometimes the bond component moved while liquidity premiums stayed flat, and sometimes it was the opposite. For brokers who only watch the bond yield and expect rates to react one to one, this is a powerful reminder that pricing is built on more than a single line on a chart, and that non hedgeable liquidity premiums can squeeze margins even when bonds look friendly. Renewal, Retention, and the Broker Concierge With a massive maturity wave in motion, Scotia has doubled down on renewal and retention. Alex outlines three key pillars: A dedicated team of mortgage renewal specialists focused solely on upcoming maturities. A digital renewal path for clients who are comfortable self serving. A dedicated broker concierge process for Scotiabank renewals where staying put is the right move. Through the concierge, brokers can refer clients directly into Scotia’s renewal team, get updates on progress, and know their clients are being looked after without needing to re underwrite an entire deal. It protects the client experience, preserves the relationship, and respects the broker’s reputation at the same time. Alex also touches on blend and extend strategies and how they are increasingly attractive for clients who locked in at peak rates and now want payment relief without a full refinance. Deepening Relationships Through Mortgage Plus One theme that runs through the conversation is just how intentional Scotia has been about using Mortgage Plus to deepen relationships—not just with clients, but with brokers as well. By tying the mortgage to day to day banking and an additional product, Scotia isn’t just protecting capital efficiency; they’re building a stickier, more holistic relationship that’s better for long term advice. For brokers, that means the clients they place with Scotia are more likely to truly “bank” there, not just park a mortgage for five years. Alex and the hosts talk about how that shows up in real life: better service, more tailored solutions over time, and a tighter alignment between broker recommendations and bank execution Broker–Bank Alignment and the SMA Model Alex also highlights how the SMA model creates alignment that’s hard to replicate. Because the structure is relationship based rather than purely transactional, Scotia can openly share challenges (like capital constraints) and co design solutions with its top broker partners—as they did with Mortgage Plus. That level of transparency created genuine buy in on the broker side. Brokers felt like they were part of the solution, not just being handed a new requirement. Over time, that’s led to stronger loyalty, higher quality submissions, and a shared focus on doing what’s best for the client while still respecting the bank’s economic realities. What Brokers Can Take Back to Their Business There are a few clear takeaways brokers can apply immediately in their own practice. First, understand your lender’s world: pricing isn’t just “bonds up, rates up.” Liquidity premiums, hedging costs, and capital rules all matter—and clients appreciate when you can explain that clearly. Second, live the products you recommend. Dean shares that moving his own mortgage and banking to Scotia changed the way he talks about the client experience, because he’s actually lived it. Finally, don’t sleep on renewals and retention. With waves of maturities coming, brokers who understand lender programs like Scotia’s concierge and renewal specialist model will be far better positioned to guide clients through the next few years. Outlook for Rates and the Mortgage Market Looking ahead, Alex leans on Scotiabank Economics: The overnight rate is expected to sit at the bottom end of the “neutral” range, with no further cuts anticipated. Modest hikes are expected later in 2026 as inflation, growth, and unemployment rebalance. He highlights that ultra low rates are usually a sign of economic stress, not something to root for, and encourages brokers to think beyond only purchase business. With huge renewal cohorts, refinance opportunities, switches, and blend and extend options, the mortgage market itself remains very active even if resale volumes soften in some regions. For brokers, the message is clear: understand how pricing really works, lean into education, and leverage strong bank partnerships like Scotia’s SMA model to deliver better advice and smoother client experiences through the next phase of the cycle. Why You Should Listen This episode is a masterclass in understanding how big-bank pricing, capital strategy, and broker partnerships actually work behind the scenes. If you’re a broker who wants to give more sophisticated advice, look beyond headline bond yields, and truly understand the forces shaping rate sheets, this conversation is essential. For weekly market updates, sign up for the ABW Tuesday Mortgage Memo . If you’re a broker considering a network change or looking to grow, reach out to us to explore how we can support your success.