10/29/2025:

BoC Rate Cut to 2.25%: The Final Move in Canada’s Easing Cycle

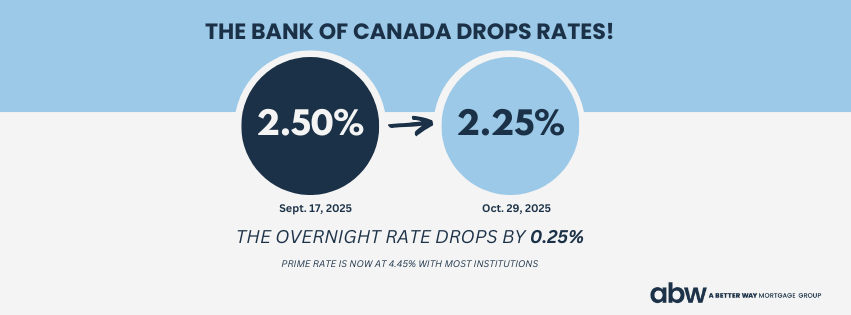

Today, October 29, 2025, the Bank of Canada (BoC) announced a 25-basis-point (bps) reduction to its benchmark overnight rate, bringing it to 2.25%—as expected by markets and signaled in recent commentary (RMG Morning Bru, Mortgage Logic News). While the cut was widely anticipated, the tone of today’s statement indicates that the central bank may now be done easing, at least for the foreseeable future. Governor Tiff Macklem stated that policy is now “at about the right level” to balance growth and inflation risks, suggesting a pause in the cutting cycle. This language sparked an immediate reaction in the bond market, with the 5-Year Canada Bond yield rising to 2.686% by late morning (CNBC Market Data).

Economic Context and Market Impact

The BoC’s decision comes amid persistent inflation uncertainty and slowing economic activity. The Monetary Policy Report revealed that Q2 GDP contracted at an annualized rate of 1.6%, reflecting the impact of trade disruptions and tariff-related business slowdowns (RMG Morning Bru). The Bank projects 1.2% GDP growth for 2025 and 1.1% for 2026, assuming no further escalation in trade tensions. Policymakers acknowledged that structural damage from U.S. tariffs has limited Canada’s productive capacity, reinforcing their decision to stop short of deeper easing (Mortgage Logic News).

Inflation remains a key concern. Headline CPI sits at 2.4%, with core measures (CPI Median and Trimmed-Mean) holding around 3.1%–3.2%. The Governing Council expects both to converge toward 2% over the next 12 months, assuming current conditions persist (RMG Morning Bru). The next inflation update arrives November 17, and markets are hoping for confirmation that both core readings have dropped below 3%.

Bond markets reacted immediately. Following the announcement, the 5-year Government of Canada yield climbed 6 basis points, while swap spreads widened slightly. Lenders are expected to hold fixed mortgage rates steady or make modest upward adjustments as funding costs rise, even as the prime rate adjusts down to 4.45%.

Impact on Borrowers

- Variable Mortgage & HELOC Holders: Prime has decreased to 4.45%, translating to approximately $15 in monthly savings per $100,000 financed. This provides modest relief for variable-rate borrowers and HELOC users.

- Fixed-Rate Mortgages: Fixed rates are expected to stabilize near recent lows but could see small increases if bond yields remain elevated this week. Brokers should watch for lender repricing between Wednesday and Friday.

- Static Payment Variable Holders: Encourage clients to reassess amortization strategies — today’s cut can slightly improve principal reduction.

- Adjustable Rate Variable Holders: Expect automatic payment reductions over the coming billing cycle.

What’s Next?

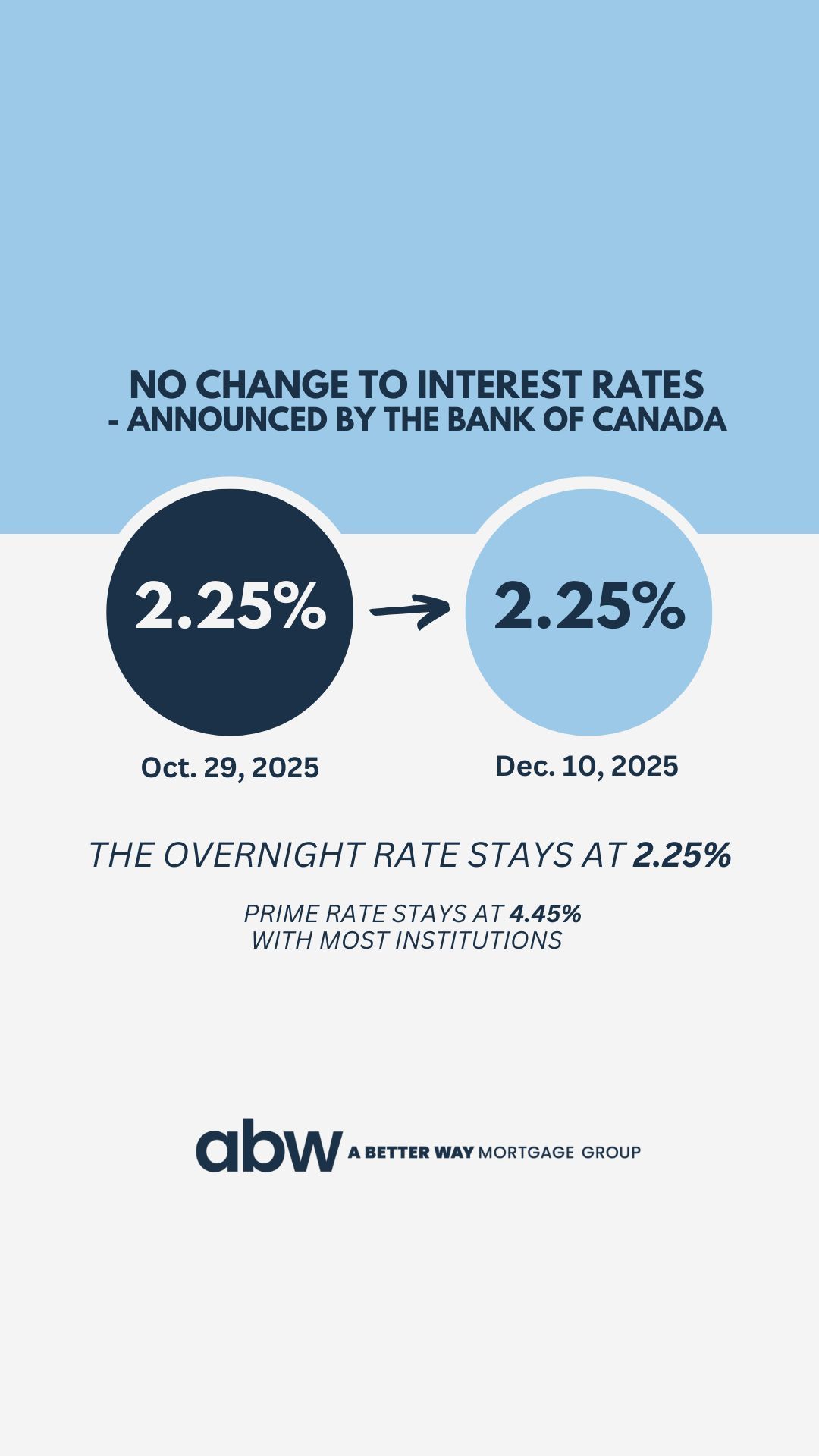

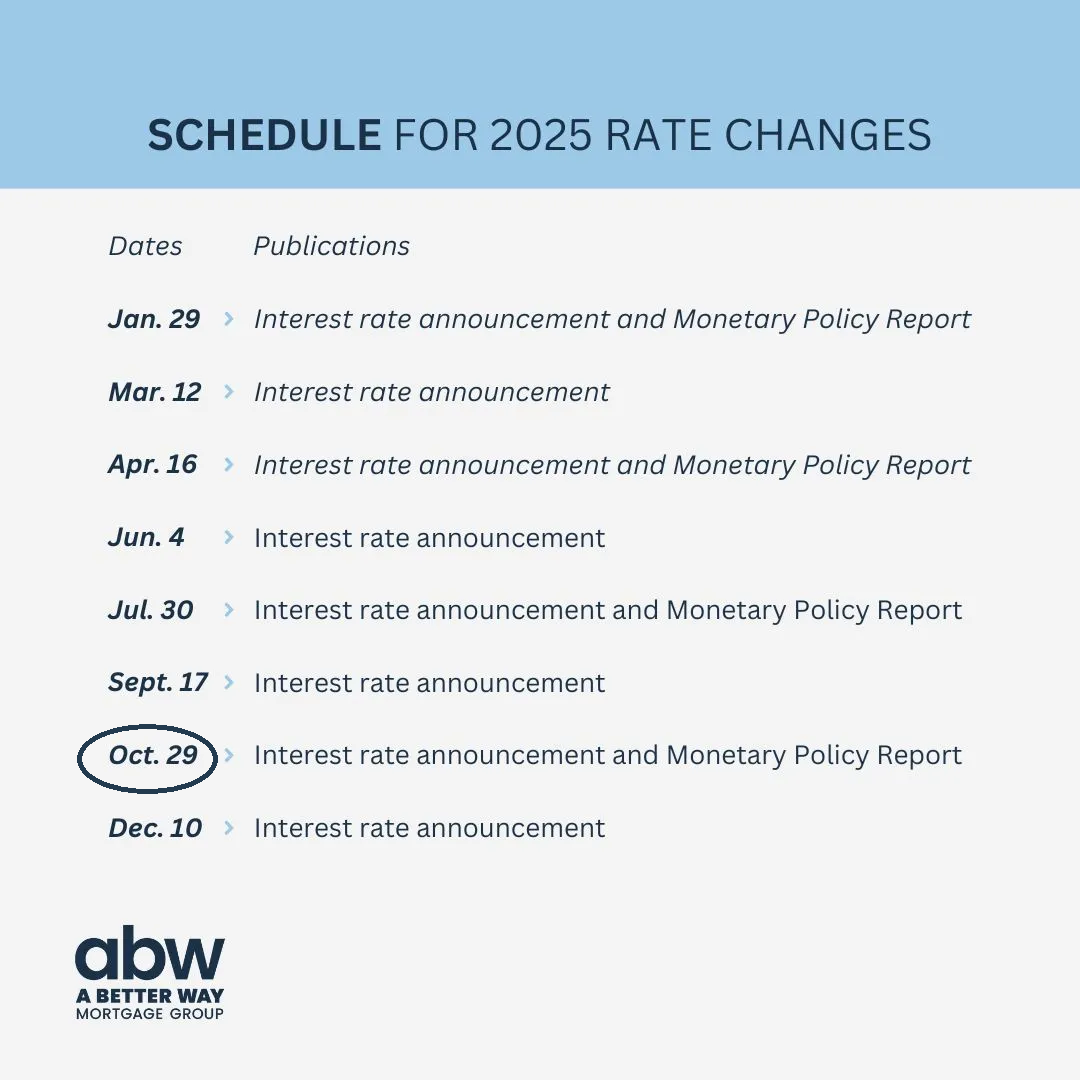

The next BoC meeting is scheduled for December 10, 2025, but market expectations for another cut are now minimal — just 10% odds priced in. The consensus view: the Bank has reached its “terminal policy rate”, barring a major economic downturn or escalation in U.S. tariffs.

Meanwhile, inflation data in mid-November will dictate sentiment heading into 2026. If CPI trends below 3%, it could mark the official start of the BoC’s stabilization phase — a shift from rate management to balance-sheet focus.

Opportunities for Mortgage Brokers

This latest cut — and the signal that it may be the last of the cycle — presents a critical moment for brokers to guide clients through the transition from easing to holding:

- Proactive Client Outreach: Update all variable-rate clients this week with customized projections. Use BoC’s statement language (“at about the right level”) to reinforce confidence and prompt early renewal discussions (RMG Morning Bru).

- Educational Content: Share simplified infographics explaining the BoC’s base economic projections — GDP growth of 1.2% (2025) and 1.1% (2026) and inflation trending to 2% — to illustrate why rate volatility may slow. Use insights from Mortgage Logic News to demystify bond yield movements.

- Targeted Marketing: Engage buyers in regions with renewed housing activity, particularly Ontario and British Columbia. Emphasize that the window of ultra-low rates may now be closing and that pre-approvals secured today could protect clients from upcoming fixed-rate adjustments.

- Renewal & Refinance Strategy: Encourage clients within 120 days of renewal to act promptly. Highlight how today’s 25-bps cut improves qualification metrics, especially for high-ratio borrowers. For those refinancing, explore debt consolidation options before yields rise further.

- Stay Ahead of the Data: Monitor upcoming inflation data (Nov. 17) and global trade updates. The next policy move will hinge on whether CPI core measures fall below 3%. Brokers should also watch the Canada 5-Year Bond (2.68%) and U.S. 10-Year Treasury (4.28%) for early signs of rate direction (Mortgage Logic News, RMG Morning Bru).

TAKE ACTION!

At ABW Mortgage Group, we’re here to help you make the most of this transitional moment. Whether you’re buying, refinancing, or renewing, our experts can guide you through today’s changing landscape.

maximize this rate cut’s benefits!

EPISODE 52: Behind the BrokerAGE with justin noda

Guest: Justin Noda

Justin Noda—A Better Way’s new Chief Compliance & Operations Officer—joins the show to launch Behind the Brokerage, a series unpacking the systems, regulations, and operational playbooks that protect brokers and power scalable growth.

With 18 years in the industry across brokering, underwriting, and leadership (ClearTrust, Origin Mortgages, The Mortgage Center, CFS), Justin explains why a true “culture of compliance” is now a competitive edge. He shares how ABW is translating complex rules—FinTrack, evolving AML expectations, and BC’s coming Mortgage Services Act—into clear, broker-friendly processes, tools, and training that make daily work easier, not harder.

Justin also outlines what the new series will cover: practical FinTrack readiness, MSA timelines and implications, inter-provincial differences (BC/AB/ON) and how to stay compliant across borders, lender relations and deal-desk ops, and why every agent should know (and use) their brokerage’s policies & procedures. Throughout, he keeps a broker-first lens—balancing regulation with real-world deal flow, client service, and efficiency.

This episode sets the tone for ABW’s next chapter: transparency, education, and operations that protect agents while elevating professionalism across the industry.

Choose to Receive the ABW Memo

This is a choice-based resource. If you'd like to continue receiving these updates weekly, please register here:

Click here to subscribe to the ABW Tuesday Mortgage Memo

We look forward to helping you stay ahead of the market in 2025.