EPISODE 56: Behind the Lender with Alex Dey, ScotiabanK

Guest: Alex Dey, VP Portfolio Optimization, Scotiabank

Hosts: Dean Lawton & Jason Marshall

In this Behind the Lender episode, Alex Dey pulls back the curtain on how Scotiabank thinks about mortgages, capital, and the broker channel. With 22 years at the bank and more than a decade focused on mortgages, Alex oversees portfolio optimization, which means keeping the mortgage book growing, profitable, within risk appetite, and capital efficient.

He explains why mortgages are considered an “anchor product” for the bank and why brokers are so central to that strategy. With roughly half of Canadians now choosing brokers, Scotiabank is committed to being present in every channel clients want to use, including branch, mobile specialists, digital, and the broker channel through the SMA model.

Pricing, Liquidity Premiums, and a Wild Year for Rates

One of the most educational parts of the episode is Alex’s breakdown of how a big bank actually prices mortgages. He explains that Scotiabank’s cost of funds has two main components:

- A base rate that tracks the bond market and can be hedged.

- A liquidity premium that reflects the extra risk the market assigns to bank funding and cannot be hedged.

In the past year, total cost of funds moved roughly ten times more than the Bank of Canada’s overnight rate changes, with sharp spikes driven by politics, trade headlines, and market sentiment. Sometimes the bond component moved while liquidity premiums stayed flat, and sometimes it was the opposite.

For brokers who only watch the bond yield and expect rates to react one to one, this is a powerful reminder that pricing is built on more than a single line on a chart, and that non hedgeable liquidity premiums can squeeze margins even when bonds look friendly.

Renewal, Retention, and the Broker Concierge

With a massive maturity wave in motion, Scotia has doubled down on renewal and retention. Alex outlines three key pillars:

- A dedicated team of mortgage renewal specialists focused solely on upcoming maturities.

- A digital renewal path for clients who are comfortable self serving.

- A dedicated broker concierge process for Scotiabank renewals where staying put is the right move.

Through the concierge, brokers can refer clients directly into Scotia’s renewal team, get updates on progress, and know their clients are being looked after without needing to re underwrite an entire deal. It protects the client experience, preserves the relationship, and respects the broker’s reputation at the same time.

Alex also touches on blend and extend strategies and how they are increasingly attractive for clients who locked in at peak rates and now want payment relief without a full refinance.

Deepening Relationships Through Mortgage Plus

One theme that runs through the conversation is just how intentional Scotia has been about using Mortgage Plus to deepen relationships—not just with clients, but with brokers as well. By tying the mortgage to day to day banking and an additional product, Scotia isn’t just protecting capital efficiency; they’re building a stickier, more holistic relationship that’s better for long term advice.

For brokers, that means the clients they place with Scotia are more likely to truly “bank” there, not just park a mortgage for five years. Alex and the hosts talk about how that shows up in real life: better service, more tailored solutions over time, and a tighter alignment between broker recommendations and bank execution

Broker–Bank Alignment and the SMA Model

Alex also highlights how the SMA model creates alignment that’s hard to replicate. Because the structure is relationship based rather than purely transactional, Scotia can openly share challenges (like capital constraints) and co design solutions with its top broker partners—as they did with Mortgage Plus.

That level of transparency created genuine buy in on the broker side. Brokers felt like they were part of the solution, not just being handed a new requirement. Over time, that’s led to stronger loyalty, higher quality submissions, and a shared focus on doing what’s best for the client while still respecting the bank’s economic realities.

What Brokers Can Take Back to Their Business

There are a few clear takeaways brokers can apply immediately in their own practice. First, understand your lender’s world: pricing isn’t just “bonds up, rates up.” Liquidity premiums, hedging costs, and capital rules all matter—and clients appreciate when you can explain that clearly.

Second, live the products you recommend. Dean shares that moving his own mortgage and banking to Scotia changed the way he talks about the client experience, because he’s actually lived it. Finally, don’t sleep on renewals and retention. With waves of maturities coming, brokers who understand lender programs like Scotia’s concierge and renewal specialist model will be far better positioned to guide clients through the next few years.

Outlook for Rates and the Mortgage Market

Looking ahead, Alex leans on Scotiabank Economics:

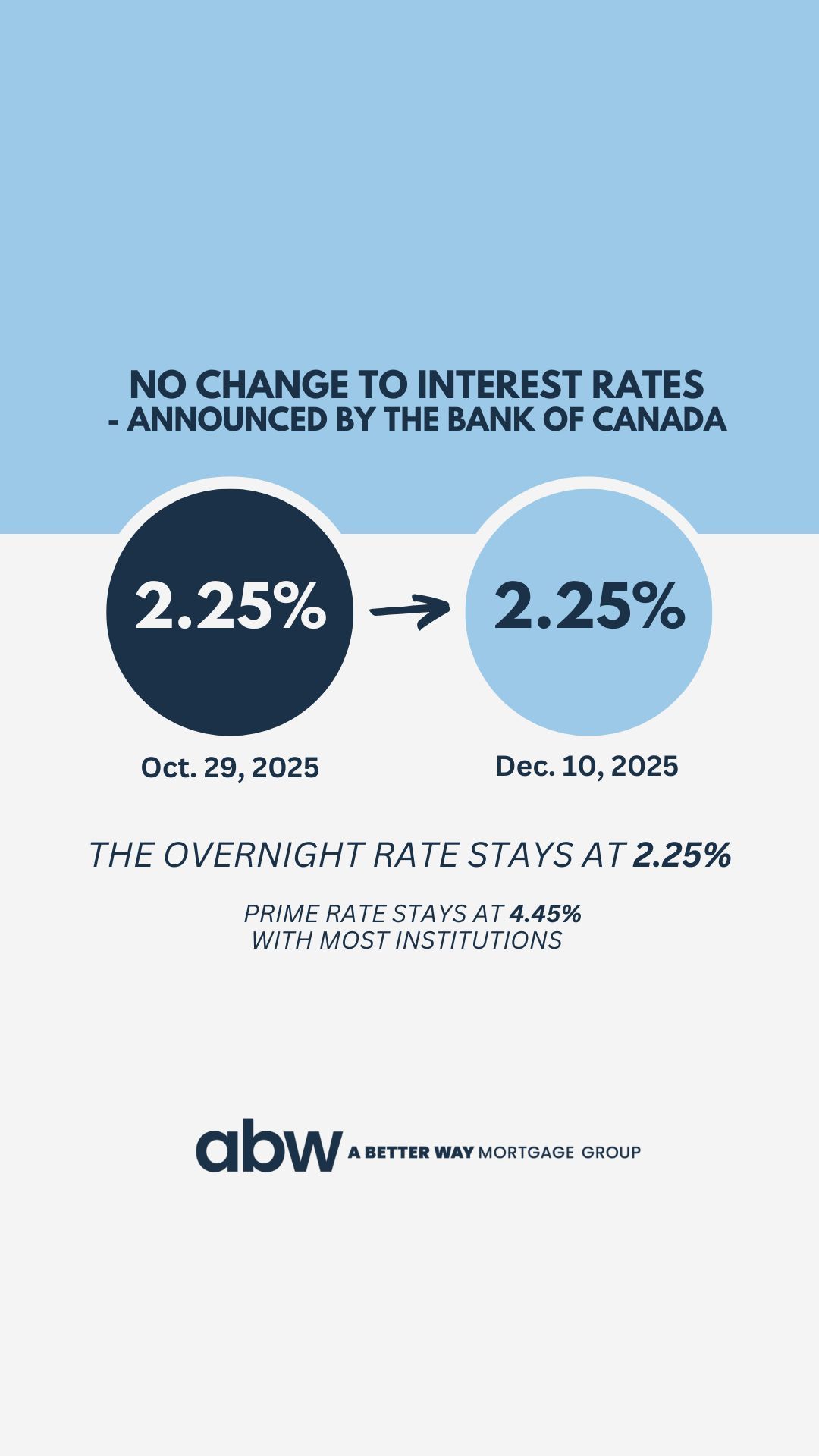

The overnight rate is expected to sit at the bottom end of the “neutral” range, with no further cuts anticipated.

Modest hikes are expected later in 2026 as inflation, growth, and unemployment rebalance.

He highlights that ultra low rates are usually a sign of economic stress, not something to root for, and encourages brokers to think beyond only purchase business. With huge renewal cohorts, refinance opportunities, switches, and blend and extend options, the mortgage market itself remains very active even if resale volumes soften in some regions.

For brokers, the message is clear: understand how pricing really works, lean into education, and leverage strong bank partnerships like Scotia’s SMA model to deliver better advice and smoother client experiences through the next phase of the cycle.

Why You Should Listen

This episode is a masterclass in understanding how big-bank pricing, capital strategy, and broker partnerships actually work behind the scenes. If you’re a broker who wants to give more sophisticated advice, look beyond headline bond yields, and truly understand the forces shaping rate sheets, this conversation is essential.

For weekly market updates, sign up for the ABW Tuesday Mortgage Memo. If you’re a broker considering a network change or looking to grow, reach out to us to explore how we can support your success.